This content is provided for informational purposes only and does not constitute financial, legal, or tax advice. Consult a qualified wealth advisor, international tax specialist, or legal counsel before making any investment decisions.

Major real estate projects and offshore developments that are redefining luxury

The offshore luxury property landscape has undergone a structural transformation since 2023. Where conventional wisdom predicted interest rate rises would uniformly dampen high-value real estate, market data reveals a bifurcation: mainstream luxury stagnated whilst the ultra-prime segment—properties commanding €5 million and above—demonstrated resilient appreciation across select jurisdictions.

This divergence reflects a fundamental recalibration in ultra-high-net-worth portfolio strategy. Offshore tangible assets now serve dual functions: wealth preservation instruments hedging against currency volatility and geopolitical uncertainty, alongside lifestyle enablement in jurisdictions offering regulatory stability.

Regulatory transparency initiatives, paradoxically, now drive capital toward compliant offshore jurisdictions rather than away from them. The OECD’s Common Reporting Standard has fundamentally altered the offshore value proposition: wealthy individuals increasingly seek legitimate tax efficiency through residency planning in stable jurisdictions, replacing the obsolete opacity model with transparency-compliant wealth structuring.

Three offshore ecosystems dominate institutional capital flows: Monaco (scarcity-driven stability), Dubai (high-growth infrastructure expansion), and Caribbean citizenship-by-investment programmes (accelerated mobility solutions). Each presents distinct risk-return profiles requiring rigorous comparative analysis beyond developer marketing narratives.

Strategic intelligence brief: the ultra-prime offshore recalibration you need to understand

- Global luxury residential prices rose 3.2% in 2025 whilst Dubai’s super-prime segment surged 25.1%—demonstrating resilience despite elevated borrowing costs.

- Monaco offers zero personal income tax for qualifying residents but commands entry pricing typically exceeding €50,000 per square metre; Dubai delivers 10-year Golden Visa pathways via AED 2 million property investment.

- Total annual ownership costs frequently reach €400,000-€500,000 for a €10 million asset, with ongoing expenses rivalling initial purchase price over holding periods.

- The OECD Common Reporting Standard mandates automatic financial information exchange across 120+ jurisdictions, fundamentally altering offshore structuring from opacity toward compliance.

- Ultra-prime liquidity constraints are material: typical sale timelines extend 12-24 months versus 3-6 months for mainstream markets.

Why wealth portfolios are shifting toward offshore luxury property in 2026

Macroeconomic orthodoxy suggested higher interest rates would universally constrain property valuations. The ultra-prime offshore segment defied this logic. Knight Frank‘s Prime International Residential Index documented a 3.2% rise in global luxury residential prices throughout 2025, marking the second consecutive year of outperformance against mainstream housing. More striking: 73 of 100 tracked prime markets recorded positive price movement, with Dubai’s super-prime tier—properties exceeding $10 million—appreciating 25.1% annually.

25.1

%

Dubai super-prime residential appreciation rate (properties above $10M) during 2025, outpacing global luxury average by factor of seven

This performance divergence signals a paradigm shift in asset allocation logic. Ultra-high-net-worth families increasingly view offshore property not as discretionary lifestyle acquisitions but as strategic wealth preservation instruments. Three catalytic forces converge: currency debasement concerns in traditional reserve economies, geopolitical fracturing driving capital mobility imperatives, and regulatory tightening in domestic jurisdictions making offshore havens comparatively attractive.

Market data reveals accelerating capital flows into jurisdictions offering political stability, tax efficiency (zero personal income or capital gains levies), and residency frameworks enabling geographic diversification. The strategic calculus has shifted from “where do you want a holiday home” to “which jurisdiction optimally balances tax domicile requirements, succession planning constraints, and portfolio diversification mandates.”

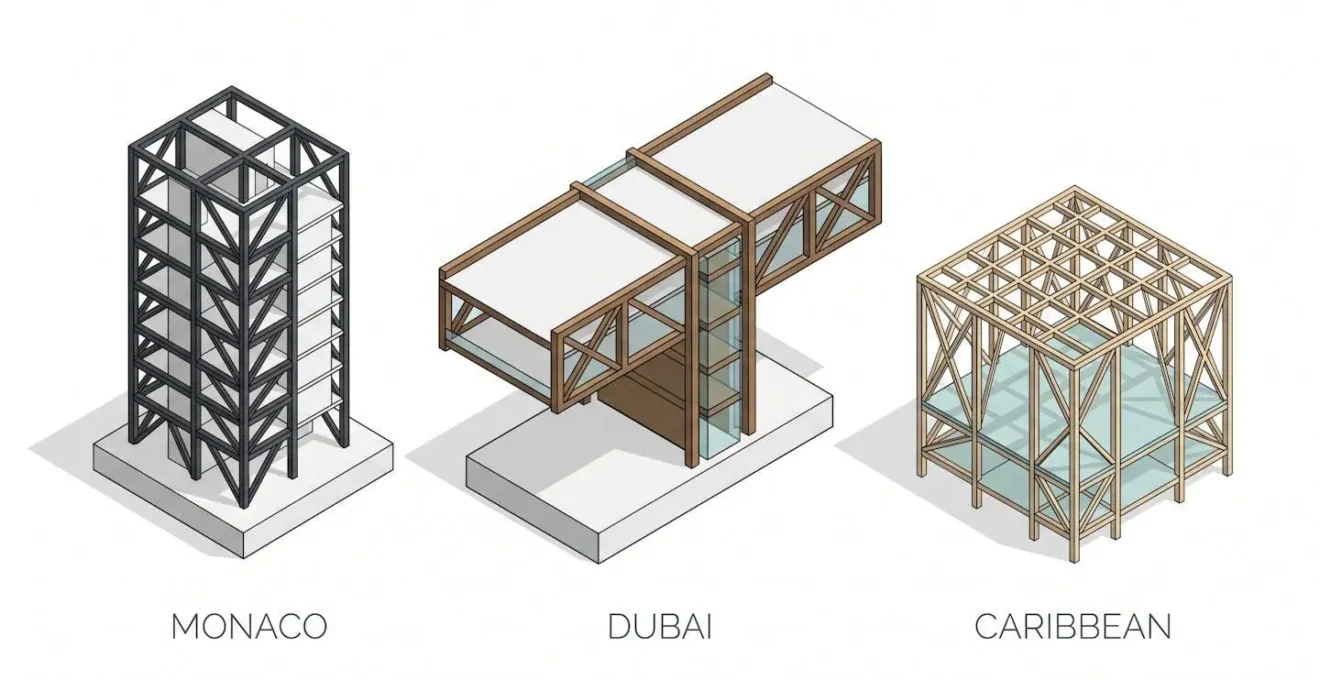

Where regulatory clarity meets architectural ambition: Monaco, Dubai, and Caribbean jurisdictions compared

Selecting an offshore jurisdiction demands systematic evaluation across tax frameworks, regulatory stability, residency pathway mechanics, market liquidity, total cost transparency, currency risk exposure, and lifestyle proposition alignment. The following tri-jurisdictional analysis isolates decision-material differences often obscured in marketing collateral.

Monaco: the zero-income-tax blueprint with finite supply

Monaco‘s value proposition rests on constitutional prohibition of personal income taxation for residents and geographic scarcity (2.02 square kilometres). This combination has generated pricing dynamics detached from conventional valuation metrics—prime districts typically command €50,000-€70,000 per square metre according to market analyses, reflecting sovereign scarcity premium rather than construction costs. Residency requires demonstrating financial self-sufficiency, securing approved housing, and maintaining 183-day annual physical presence. The framework suits investors prioritising absolute political stability and multigenerational wealth transfer planning. Limitations include minimal rental yield potential—typically 1-2% gross returns—and substantial upfront capital requirements extending beyond purchase price.

Dubai: freehold ownership meets zero capital gains liability

Dubai‘s regulatory trajectory since 2002 freehold reforms has systematically dismantled foreign ownership barriers whilst constructing investor protections. The 2019 Golden Visa introduction—offering 10-year renewable residency via AED 2 million (approximately €500,000) property investment—catalysed unprecedented capital inflows. Official data from the April 2026 GDRFA-DLD platform reform reveals 158,000 Golden Visas were issued during 2023 alone, nearly doubling the prior year’s volume. The tax architecture offers compelling advantages: zero personal income tax, zero capital gains liability, zero inheritance tax. Rental yields in luxury tiers commonly range 4-5% gross annually—materially exceeding Monaco’s returns. Dubai’s proposition aligns with investors seeking yield-generating assets and rapid residency processing (often 60-90 days).

Caribbean citizenship-by-investment: tax efficiency at lifestyle cost?

Caribbean jurisdictions—principally St. Kitts & Nevis, Antigua & Barbuda, and Dominica—offer citizenship via real estate investment routes. Minimum thresholds typically range $200,000-$400,000 for government-approved developments, with processing timelines of 3-6 months representing the fastest path to second passport acquisition globally. The tax proposition is absolute: zero worldwide taxation for non-resident citizens. Limitations are material: luxury inventory depth cannot rival Monaco or Dubai, and resale liquidity is constrained. Industry consensus increasingly points to Caribbean CBI as niche diversification play—a second passport insurance policy—rather than primary offshore property strategy.

| Criterion | Monaco | Dubai | Caribbean CBI |

|---|---|---|---|

| Purchase price entry (luxury tier) | €5M-€10M+ | €1.5M-€3M | $200K-$400K |

| Income tax (residents) | 0% | 0% | 0% (non-residents) |

| Capital gains tax | 0% | 0% | 0% |

| Residency pathway timeline | 4-6 months | 60-90 days | 3-6 months (citizenship) |

| Minimum stay requirement | 183 days annually | None (visit biennially) | None |

| Rental yield potential | 1-2% gross | 4-5% gross | Variable (2-4%) |

| Resale liquidity (typical timeline) | 12-18 months | 6-12 months | 18-36 months |

| Currency risk (EUR investor) | Minimal (EUR zone) | Moderate (AED/USD) | Moderate (USD/XCD) |

Flagship developments rewriting the luxury rulebook: architectural case studies

Paradigm-shifting projects distinguish themselves through architectural pedigree, sustainability integration, and experiential innovation. Monaco’s Mareterra development represents the principality’s first territorial expansion in two decades. Renzo Piano Building Workshop’s design prioritises environmental integration—the land reclamation incorporates marine ecosystem regeneration zones, district-wide seawater cooling systems, and photovoltaic integration achieving near-net-zero operational energy. Dubai’s Royal Atlantis Residences illustrates experiential maximalism with sky pools featuring transparent bottom panels and celebrity chef restaurants. LEED Platinum certification mandates measurable performance across energy efficiency and materials sourcing. Industry data suggests LEED Platinum-certified luxury properties command 8-12% resale premiums versus non-certified comparables, reflecting operational cost savings and alignment with institutional investor ESG mandates.

The hidden calculus: total ownership costs and liquidity realities

Developer marketing systematically foregrounds purchase price whilst obscuring ongoing cost structures. Rigorous investment analysis demands quantifying annual service charges, opportunity cost on deployed capital, financing expenses, currency hedging, and compliance obligations. For a €10 million Monaco apartment, purchase transaction costs typically add 7-10%. Annual service charges in full-service developments commonly represent 2-4% of property value—€200,000-€400,000 yearly. Opportunity cost merits acknowledgement: €10 million deployed in property generates negligible yield versus 3-4% available in money markets—a €200,000-€300,000 annual differential. Understanding types of risk in investments specific to illiquid luxury property requires distinguishing market risk from regulatory and currency risk. True annual costs for a €10 million property plausibly reach €450,000-€550,000, compounding to €4.5-€5.5 million over ten years.

Liquidity trap: the 12-24 month reality

Ultra-prime segment liquidity constraints are material and systematically underestimated. Typical sale timelines for properties exceeding €5 million extend 12-24 months versus 3-6 months for mainstream markets. Monaco’s property market operates with substantial off-market activity, creating information asymmetry for independent buyers. Accessing this requires established relationships with specialist agencies focusing on luxury real estate in Principality Of Monaco such as John Taylor, which maintain exclusive developer and seller networks in prime districts including Carré d’Or and Fontvieille. Bypassing this expertise typically extends search timelines by 6-12 months and risks overpaying due to limited comparable transaction visibility. Forced-sale scenarios routinely incur 10-20% discounts to achieve transaction velocity.

-

Independent surveyor report confirming valuation and identifying latent defects

-

Total annual cost projection aggregating service charges, taxes, and opportunity cost

-

Comparable transaction analysis from recent sales in same development

-

Developer financial stability verification including completion guarantees

-

Exit liquidity assessment documenting historical sale timelines

Structuring acquisition: SPVs, trusts, and CRS reporting obligations

Ownership structuring decisions cascade into multi-decade tax, estate planning, and compliance consequences. Three primary frameworks warrant evaluation: direct personal ownership, special purpose vehicle structures, and trust arrangements. Each presents distinct trade-offs between simplicity, tax efficiency, asset protection, and reporting complexity. For those new to cross-border structuring, consulting a beginner’s guide to real estate investing provides foundational concepts before engaging specialist offshore counsel.

Direct personal ownership offers administrative simplicity but minimal tax optimisation. The OECD‘s Common Reporting Standard mandates that financial institutions in participating jurisdictions obtain and automatically exchange financial account information annually—a framework now encompassing 120+ jurisdictions. Privacy and tax compliance are no longer conflicting objectives but parallel requirements.

SPV ownership historically provided anonymity benefits now substantially eroded by beneficial ownership registries. Monaco, Dubai, and most Caribbean jurisdictions maintain registers accessible to law enforcement and tax authorities. The structure retains utility for estate planning and potential corporate tax optimisation, though the latter demands sophisticated structuring. Trust structures offer robust asset protection but introduce complex reporting obligations under both FATCA and CRS frameworks.

The regulatory trajectory strongly favours early voluntary disclosure and compliant structuring. Investors domiciled in high-scrutiny jurisdictions face elevated audit risk, with tax authorities increasingly cross-referencing CRS data against declared assets. The operational imperative: engage qualified international tax counsel and STEP-qualified advisors before acquisition.

Inherent limitations of generalised guidance:

- Tax treatment varies dramatically by investor domicile and target jurisdiction; generic guidance cannot replace personalised tax planning.

- Regulatory frameworks evolve continuously; information may become outdated between publication and your decision timeline.

- Property valuations in ultra-premium segment lack transparent comparables; independent appraisal essential to avoid overpayment.

- Residency-by-investment programmes remain subject to policy changes and potential termination.

Explicit risks requiring professional mitigation:

- Misalignment between investment structure and tax residence may trigger unexpected liabilities or compliance failures.

- Overreliance on developer projections without independent due diligence may result in overpayment or liquidity constraints.

- Failure to satisfy ongoing residency requirements may invalidate tax benefits or residency status.

- Currency mismatch introduces exchange rate risk requiring hedging strategies—unhedged positions can erode returns significantly.

Qualified advisors you must consult before commitment:

International tax counsel specialising in cross-border structuring, independent property surveyor, wealth structuring advisor (STEP-qualified), and immigration lawyer with jurisdiction-specific residency programme expertise.